Top Server Companies in the World

Table of Contents

The worldwide server market value declined in 2020 due to the COVID-19 crisis, but it is expected to gain pace in 2021. The server market is dominated by Chinese and American companies, where China has a higher market share.

1 . Leading Server Companies

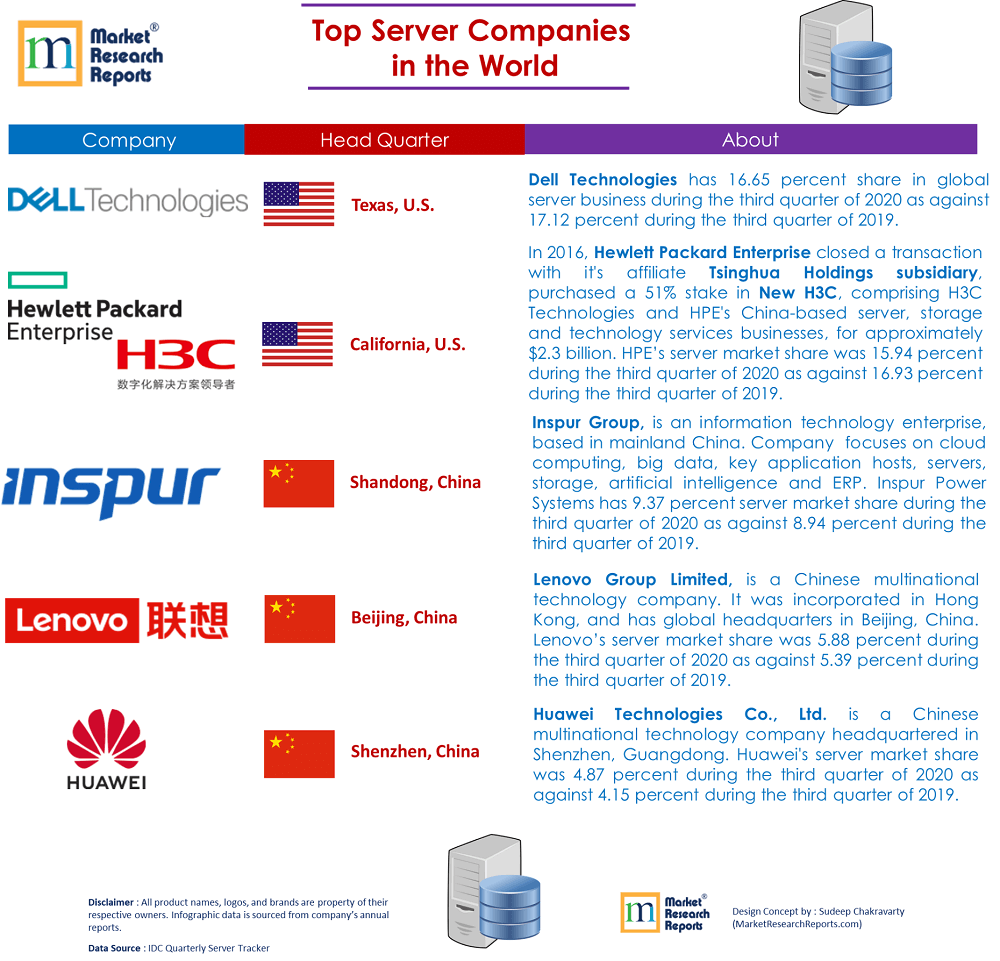

- Dell Technologies

- Hewlett Packard Enterprise

- Inspur Group

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

Within the worldwide server market, the competition is growing. The Original Equipment Manufacturers (OEM), which are branded hardware companies, and Original Design Manufacturers (ODM), which manufacture and assemble the components for OEMs are standing face to face. ODMs use technical specifications from OEMs to produce the custom product, but ODMs may also pitch in their products directly to buyers, which are popular as “White Boxes.” White boxes are computing hardware systems that do not carry a brand name and model number and are only built for specific customers as per their configuration.

According to IDC Quarterly Server Tracker vendor revenue in the server market grew 2.2 percent to USD 22.6 billion during the third quarter of 2020, while the ODM Direct group of vendors accounted for 28.0% of total server revenue, up 8.4% year over year.

2 . Impact of COVID-19 on Global Server Market

The global server market is witnessing a trend where the hyperscalers are bypassing the OEMs and buying servers directly from the ODMs. Most of the hyperscalers have started favoring these ODMs instead of OEMs for cost-benefit, which is resulting in the commoditization of server products thus leading to decline in prices and overall margins.

Global Servers Market Outlook analyses the current trends, drivers, and challenges impacting the servers market. The report also presents the revenue opportunities in the servers market through to 2024, highlighting the market size and growth by region, product type, vertical and size band.

OR

Servers provide uninterrupted services for servers running networking, databases, system applications, etc. These servers enable the latest security advances and are scalable to support the growth of mission-critical applications. They also provide enterprise-class features with high availability, uninterrupted access to systems and data, full-function server operating systems, etc.

Economic slowdown due to COVID-19 has driven down enterprises’ server spending in 2020. Most enterprises have experienced a significant revenue loss in 2020 due to the COVID-19 disruptions. Many enterprises have already cut their 2020 ICT spending, which is likely to impact the demand for servers.

Spending on server upgrades especially are likely to take a hit as enterprises adopt the wait and watch strategy and make do with available servers amidst the crisis. According to an enterprise ICT Investment trends survey carried out in mid-2020, about 66% of the respondents claimed that their enterprises would see their revenue decline in 2020 compared to the previous year. Meanwhile, about 58% of the surveyed respondents claimed that their enterprises would decrease their intended IT budgets in 2020 following the coronavirus outbreak.

Related Reports

Global and Cloud Server Market Size, Status and Forecast 2020-2026

Global Edge Server Market Research Report 2020

Global Rack Servers Market Report 2015-2026, Market Size, Competitive Landscape, Regional Outlook and COVID-19 Impact Analysis

Global Micro Servers Market 2020 by Company, Regions, Type and Application, Forecast to 2025

Global Server System and Server Motherboard Market Size, Manufacturers, Supply Chain, Sales Channel and Clients, 2020-2026

Related Industry Articles

1. Equinix, Digital Realty and NTT Data Centres Ltd are becoming the largest Data Centre Providers in World

2. Top 10 Emerging Countries for Public Cloud and Data Centre Market

Article Sources:

infotechlead.com/networking/server-share-of-dell-hpe-inspur-lenovo-and-huawei-in-q3-64287

jpmorgan.com/content/dam/jpm/commercial-banking/documents/equipment-financing/EquipmentInsightsNewsletter_Technology_FNL_ADA.pdf

marketresearchreports.com/globaldata/global-servers-market-outlook-2024

jpmorgan.com/content/dam/jpm/commercial-banking/documents/equipment-financing/EquipmentInsightsNewsletter_Technology_FNL_ADA.pdf

marketresearchreports.com/globaldata/global-servers-market-outlook-2024

About The Author